Former Finance Minister, Seth Terkper, says Ghana’s total debt stock published by the Bank of Ghana does not reflect the true debt of the country.

Mr. Terkper argues that Ghana’s debt to GDP is currently 63 percent unlike and not the 59.3 percent published by the central bank.

The Bank of Ghana in its Summary of Economic and Financial Data pegged the country’s total debt stock by March 2020 at 236.1 billion cedis, representing 59.3 percent of the GDP.

But speaking to Citi Business News, the former Finance Minister said the figures have been under-reported.

“They used the GDP figure that was used in the 2020 budget to express the new level of debt as percentage of GDP and that gives you 59.3 percent,” he said.

He pointed out that the figure is different from what was presented to the IMF which puts Ghana’s debt 236.1 billion cedis. Mr. Terkper said the Bank of Ghana should have published the debt stock as was presented to the International Monetary Fund recently when government applied for the IMF’s emergency COVID-19 fund.

“The Public Debt cannot be 59.3 percent at end-March 2020 unless GoG is keen to continue the controversial “parallel” fiscal reporting that it denies” Mr. Terkper stressed in an article.

Criticizing government, he warned that misreporting debt figures will not only create policy credibility issues, but will also throw the budget out of gear since the economy will not be able to support projections made by government.

“The issue is key since it affects financing of the Budget that Parliament approves—as an outcome of the budget deficit, borrowing and amortization of debt,”.

Below is the full article

BOG MAY 2020 MPC STATEMENT

PUBLIC DEBT HIGHER THAN BOG’s 59.3 PERCENT:

CAN’T DEFY GRAVITY WITHOUT BOG

Seth E. Terkper

[Former Minister for Finance]

Introduction

The Bank of Ghana (BOG) Monetary Policy Committee (MPC) Report for May 2020 curiously puts the end-March 2020 public debt at 59.3 percent. Since the 2019 Debt Report and the IMF show the end-2019 debt level as 63 percent, it is unlikely to decline substantially to 59.3 percent. BOG’s itself observes a revenue shortfall, higher expenditures, high borrowing (e.g., US$3 billion bond; loans of US$230 million and domestic bonds), and slowdown in GDP. The fiscal section of the MPC Statement reads verbatim as follows.

“Provisional data for the first quarter on the execution of the budget show a widening of the deficit relative to what was observed for the same period in 2019. As at the end of the first quarter, a deficit, equivalent to 3.4 percent of GDP has been recorded compared with a deficit target of 1.9 per cent of GDP.

“The larger deficit is explained by shortfalls in tax revenues—on the back of shortfalls in international trade taxes, taxes on goods and services and taxes on income and property in response to unfavourable external and domestic conditions—and higher pace of spending, which included some unbudgeted COVID-19 related expenditure.

The expanded deficit led to an increase in the debt stock to 59.3 percent of GDP at the end of March 2020” (emphasis added).

The Public Debt CANNOT be 59.3 percent at end-March 2020 unless GOG is keen to continue the controversial “parallel” fiscal reporting that it denies. The MPC statement may not include the “exceptional” expenditures that Ministry of Finance (MOF) now includes in only footnotes. However, it is worth discussing in a banking context, even if the fiscal data and text are from MOF since they relate to the Consolidated Fund and other Public Accounts at BOG—unless some MOF records do not form part of the Treasury Single Account (TSA) initiative and, therefore, not visible to BOG.

The issue is key since it affects “financing” of the Budget that Parliament approves—as an outcome of the budget deficit, borrowing and amortization of debt. Other sections discuss BOG “zero-financing” and “fiscal dominance” rules, which were performance criteria under the 2014-2019 Enhanced Credit Facility (ECF) Program. At the time, the background of sustained global crisis (2008 and 2014), disruption in gas supply from Nigeria, and single-spine wage (budget) overruns did not seem to matter.

Why Public Debt cannot defy gravity

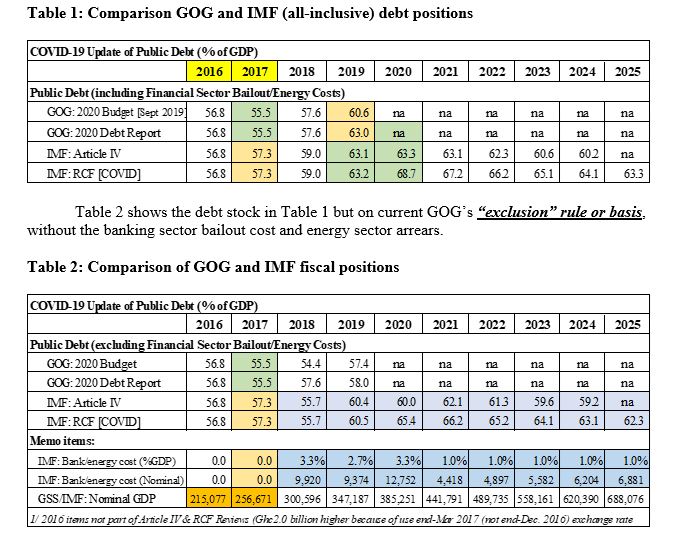

A key aspect of fiscal reporting since 2017 is exclusion of “exceptional” expenses from the budget deficit (or fiscal balance) and public debt but adding “exceptional” receipts. The main items omitted are bank bailout costs and energy sector arrears, payable from ESLA levy proceeds and bonds. Thr GOG “exclusion” rule is the only plausible explanation for public debt decreasing between end-December 2019 and end-March 2020.

Public debt at 60 percent at end-2019

Table 1 (all-inclusive) and Table 2 (exclusion) bases show GOG’s parallel numbers, as compared with the IMF positions in recent Article IV (2019) and Rapid Credit Facility or RCF (2020) Reports. Table 1 shows the “all-inclusive” rule for debt-to-GDP ratio that Ghana has in its fiscal framework since the 1980s.

A comparison between IMF and GOG after 2020 is not possible since only the Fund gives estimates of energy arrears and bank bailout costs to 2025. Nonetheless, some figures are derived, to help make the case that BOG’s end-March 2020 debt stock is very conservative.

GOG has no projections from 2020 but its end-2019 “all-inclusive” outcomes for end-2019 exceed 60 percent.

Even under the “exclusive” basis, GOG’s loans from January to March 2020 exceed the conservative 1.3 percent (59.3 less 58 percent) increase in the debt stock.

For example, the February US$3 billion Sovereign Bond alone [at US1=Ghc5.75] is 4.24 percent of GDP [2020 = Ghc385.3 billion].

Even assuming half of the Bond value was for refinancing (replace old debt], the other half increases the debt stock by 2.24 percent, not 1.3 percent.

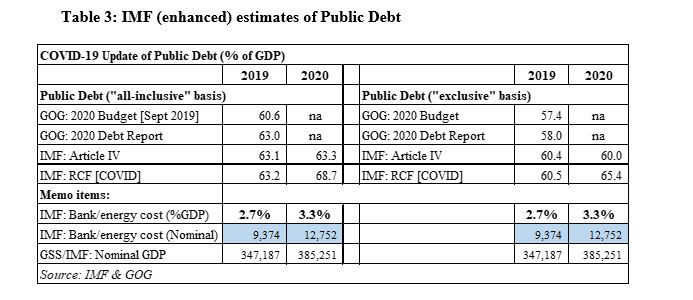

As Table 3 shows for only FY2019 and FY2020, IMF’s provisional debt stock for end-2019 and elevated projections for end-2020 make the conclusions credible:

BOG’s MPCs narrative does not support a decrease

BOG’s own narrative of slow growth rate, falling revenues, and higher expenditures, and conclusion of a wider budget or deficit does not support a decline.

On the contrary, the rational conclusion from the narrative from Section 1 points to a higher debt stock in 2020 (Qtr 1) against the benchmark 60 percent for 2019.

The elements point to lower GDP (denominator) and higher borrowing pressures on debt (numerator).

The IMF’s Article IV and RCF [COVID-19] Reports, which GOG approved, give better guidance on the likely future impact (on deficit or fiscal balance and debt) of the banking and energy sector costs, and warning on contingent liabilities (GOG quasi-fiscal guarantees).

Government’s 2020 (Qtr 1) borrowing does not support a decline

The significant early COVID-19 “front-loading” of known borrowing in Quarter 1 of 2020 and macro-fiscal factors (section 2.2) suggest elevated risk of public debt distress.

2020 Sovereign Bond: as noted, February 2020’s US$3 billion Sovereign Bond alone [at US1=Ghc5.75] is 4.48% of GDP [2020 = Ghc385.3 billion].

Net Bond proceeds: Assuming half of the Bond refinanced or replaced older debt, the balance increases the debt stock by 2.24 percent, not 1.3 percent.

Standard loans: Parliament approved about €1.27 billion and US$207 million loans (equivalent to Ghc9.22 billion)—adds to debt stock and disbursements to the Budget.

Domestic Bond Calendar: GOG planned to “issue a gross amount of Ghc19.09 billion, of which Ghc15.69 billion is to rollover maturities and the remaining Ghc3.40 billion is fresh issuance to meet GOG’s [Budget] financing requirements.

The

Further, GOG and IMF agree to classify the RCF (COVID-19) quota-full US$1 billion concessional loan approved in April 2020 as budget, not BOP, support. Together with other loans, this will elevate the frontloading and debt situation and worsen the risk of debt distress.

Debt could exceed 70 percent of GDP

The trajectory for public debt at the end of 2020 is worrisome as the Corona Virus crisis merely adds to existing financing pressures. A prolonged COVID-19 crisis will add to borrowing pressures, worsen the large financing gap, and push the ratio beyond 70 percent.

IMF estimates: in the RCF (COVID-19) Report in March 2020, the Fund puts the debt-to-GDP ratio at 68.7 percent (all-inclusive basis) and 65.5 percent (exclusive) basis.

Fitch’s more gloomy estimates: The ratings agency forecasts the 2020 debt ratio at 76.8 percent, “owing to the combination of a wider fiscal deficit and cedi depreciation … debt would equal 535% of government revenue, twice the ‘B’ median of 214%”.

The fiscal gap exists with three (3) oilfields, not one (1), from 2017; output is up from 70,000 barrels per day (bpd) to nearly 190,000 bpd; price increase above US$60 pbl from sub-US$40s pbl; and gross revenue quadrupling o above Ghc4 billion from less than Ghc1 billion.

Conclusion

The projection for public debt is an increase from 56.85 percent to 76.8 percent from end-2016 and end-2020—on new rebased GDP (2013) and revenues rising from one (1) to three (3) oil fields. The BOG MPC Statement notes:

“Preliminary assessments show that the financing gap that was estimated at the time of applying for the IMF RCF in March 2020 has widened significantly, resulting in a large residual financing gap. Current market conditions, in the wake of the pandemic, will not allow the financing of the (fiscal) gap from the domestic debt capital markets without significantly increasing interest rates.

Hence, BOG seems motivated to intervene with fiscal management with extraordinary powers in the BoG Act, 2002 (Act 612), as amended, on the basis of high interest rates only. Under section 30, it proposes to “increase the limit of BOG’s purchase government securities in the event of any emergency to help finance the residual financing gap.” Unlike the RCF, the MPC does not differentiate between the pre-COVID-19 and post-COVID-19 fiscal gap.

BoG seems to finance the 2020 Budget directly: “Today, under the BoG’s Asset Purchase Programme (APP), the Bank has purchased a GoG COVID-19 relief bond with face value of Ghc5.5 billion at the MPC rate with a 10 year tenor and a moratorium of two (2) years (principal and interest). The Bank stands ready to continue with its APP up to Ghc10 billion in line with the current estimates of the financing gap from the OVID-19 programme”.

In deficit-financing terms, the Bank’s option is likely to have been newer (not existing or old, as is financial crisis practice) Ghana COVID-19 Relief Bonds with generous debt service terms. In subsequent articles, we will explore and discuss the “fiscal gap” and argue that a large percentage existed before COVID was declared a global emergency.

Source: Citibusinessnews.com